People often ask me how much money a frum family needs to live. “Just give me a ballpark figure for a family of X living in Community Y,” they say. It’s definitely an important question to consider, but unfortunately, it’s impossible to answer it wisely on one foot. There’s just too much variability in a frum family’s budget, even after we factor in differences in family size and location.

3 Newlywed Couples, 3 Unique Budgets

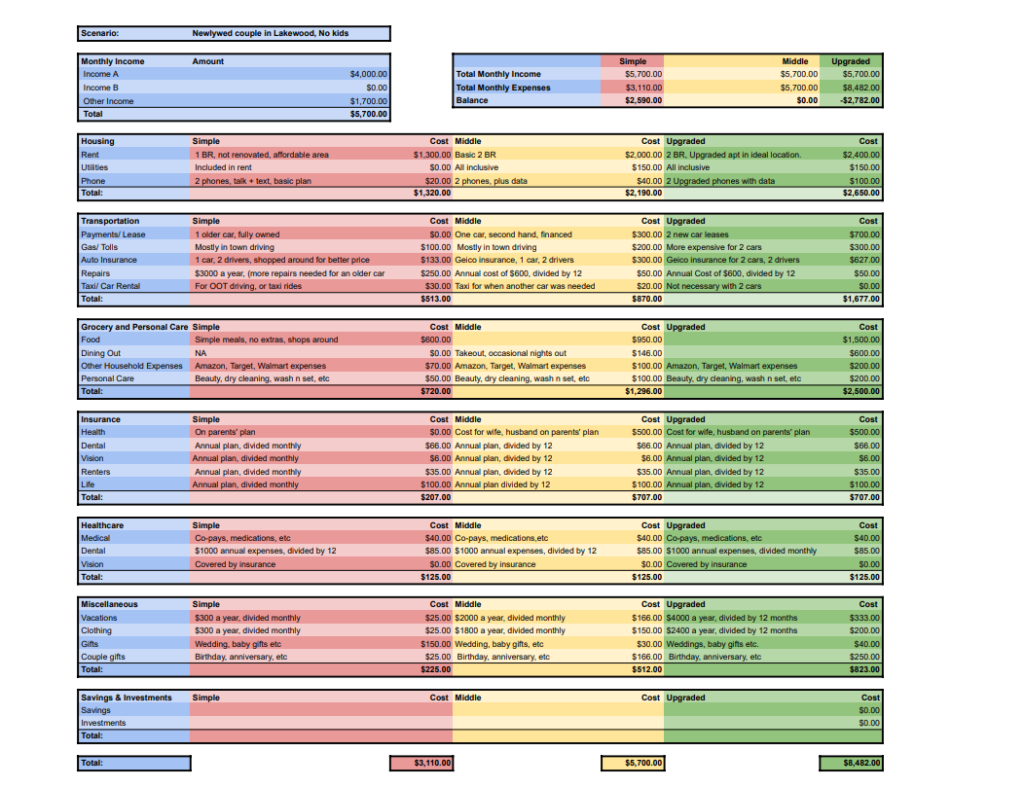

To illustrate this vital point in the most vivid and impactful way, I had my trusty GeltGuide editor, Malka Michalowicz, prepare realistic budgets for three Shanah Rishonah couples living in Lakewood.

As a fairly newlywed herself, she was able to get actual data from real couples by polling her friends. After double-checking for outliers, we still end up with three vastly different numbers.

A family living simply may be spending $2,995 a month, those spending a bit more on upgrades come in at a monthly $5,700, while there’s a significant segment that can be spending as much as $8,500 a month!

On an annual basis, we are talking about a difference in the tens of thousands of dollars.

See the chart, (or click here to view it in a larger pdf) and then below, we will discuss each category a bit. It’s clear that even without any super extravagance, you can easily double or triple your spending in any category.

Housing Is Huge

Simple: $1,320

Middle: $2,190

Upgraded: $2,650

As a newlywed kollel couple, my wife and I were thrilled to find a small one-bedroom within blocks of Beth Medrash Govoha. While small, these apartments were and still are among the most affordable options in Lakewood. Even then, though, there was a small but growing trend to rent two-bedroom basement apartments a bit further out. You spent more but enjoyed far more space. The “bessere menschen” rented the small but relatively pricey townhouses near the lake or in Coventry Square.

As you can see on the chart, there are three common housing levels today, too, with large cost disparities between them. There is no right or wrong, but they are very different.

Transportation Trade-offs

Simple: $513

Middle: $870

Upgraded: $1,677

Living near your kollel (and/or your spouse’s job) also means you can get by with just one car. Transportation is a far smaller cost than housing, but it’s still pretty substantial, especially if you go the ravchus route—almost unheard of twenty years back—of leasing two brand-new vehicles.

Whether to get a cheap clunker that will require ongoing repairs or a solid secondhand car is both a financial and menuchas hanefesh question. There is no clear right or wrong answer here either, just differing perspectives on the trade-offs.

Food: From Frugal to Fresserei

Simple: $720

Middle: $1,261

Upgraded: $2,500

Food finance is a bit nuts. We have an article coming up, showing how even shifting to a simpler or fancier menu, cooked at home, can have a significant impact on annual budgets.

Also, many people shop for food with little attention to variations between stores and brands. The cost differential between the options can easily be 20–50% for the exact same items! The same applies to household dry goods, such as toiletries, cleaning supplies, and plasticware.

Once you start mixing in takeout and restaurants, food budgets can “mushroom” drastically (excuse the corny puns).

Insurance + Healthcare + Uncle Sam = Bleak Options

Simple: $332

Middle: $832

Upgraded: $832

Health insurance has become a major cost factor in the United States. This reality is also why vast chunks of America have their first experiences with the bleak realities of government programs.

The value of “free health insurance” from Medicaid can be many thousands of dollars annually. In Lakewood, this “free” coverage is often superior to the eye-wateringly expensive private health insurance options!

It’s beyond the scope of this article to discuss the myriad ripple effects of these government policies, beyond saying the numbers and consequences are far too significant and widespread to ignore today.

Miscellaneous, AKA the Fun Stuff

Simple: $110

Middle: $547

Upgraded: $898

Some Shanah Rishonah couples, coming out of the shopping sprees common for chassan bachurim and kallah maidlach, will make do in the clothing category for YEARS! Others, more attentive to never-ending style changes and also subject to inevitable post-marriage body changes, may spend quite a bit here.

The same applies to gifts. Having gotten into a cycle of gift-giving to build their budding relationships, some young couples dig deep into their savings to continue lavishing material displays of love and devotion on each other. Others may mutually agree that the days of expensive gifts are over for now. Instead, they channel their savings into building nest eggs for a home down payment rather than more trinkets and baubles.

Vacation Vanities

Simple: $300 (ANNUALLY)

Middle: $2000 (ANNUALLY)

Upgraded: $4000 (ANNUALLY)

I know young couples whose idea of a vacation is squishing into their parents’ bungalow and having ice cream in Woodbourne. Cost: $100. I also know young couples spending fortunes exploring the world together. Each considers the other quite meshuga for their “ridiculous” approach to getting a refreshing change of scenery. Who’s “right”?

Neither. Though I do have my personal preferences and opinions here (actually, in all these categories), personal finance is personal—barring issurim or extremes. Couples should do what works for them.

“Free” Vacations?

One thing that does irk me is when people convince themselves that using credit card miles makes travel free. Money is fungible, and the numbers speak for themselves.

You can just as easily have your credit card spending converted to cash, or save your miles for “must-travel” instead of “fun” travel. Credit card usage also very often leads to greater spending and, in the worst case, to paying costly interest when the miles game doesn’t go as planned.

Taxes

I left out taxes because there are so many relevant factors to the ultimate cost. But as we alluded to when discussing government programs, the shifts in the bottom-line numbers can be substantial.

People earning high salaries are often frustrated and confused as to why they don’t have more spending power. But the nature of our tax system is: the more you earn, the more you pay. Sometimes it really is not worth it to kill yourself to bring in that extra money.

Massive Money

So there you have it, black and white. If we assume these three couples are bringing in the same amount of income—$4,000 a month from a salary and $1,700 from parental support—you can either end up with a significant amount of savings or a deficit, depending on your spending.

Monthly Balance (Income-Expenses):

Simple: $2,705

Middle: $0.00

Upgraded: -$2,857

Carry that out over five years, and you can understand why one couple has a massive down payment ready to go, and another is totally broke!

Can Be Wider Still

Note also that we are not even discussing the extremes on either side. There will be a percentage who are super frugal, and on the spending side, there’s obviously no upper limit, in theory, to what someone might spend. Income will also vary.

We believe our little survey captures the broad majority of the population—say, the 25th through the 75th percentiles or something like that.

Especially Down the Road

And this analysis focuses on couples with the fewest moving parts. Start adding in much larger families, tuition, daycare, therapy, student loans, mortgages, and other costs of large families, and you literally have shifts not in the tens of thousands but hundreds of thousands annually.

You Do You

Budgeting is about awareness of trade-offs; there are few rights or wrongs beyond the simple reality that you need to live within your means to avoid ending up in debt. By saving and investing, your future may be far more comfortable than the extra indulgences you enjoy now.

Every couple needs to recognize that they do have a lot of control over many aspects of their budgets, and it is their responsibility to consider the trade-offs.

Controlling Costs Is Crucial

Hopefully, this article vividly highlights that even relatively small adjustments to your lifestyle can have a massive financial impact over time. Don’t think for a moment that your spending decisions don’t matter.

And if you don’t have some spending discipline, those numbers will likely spiral indefinitely.

Want to dig deeper?

Try these related articles

Starting off Your Marriage on the Right Financial Foot

Young and Loaded: Building Financial Discipline During Times of Abundance