Yehuda Strassberg was concerned about his real estate investments. He’d done well at first after entrusting his savings to a fellow who invested in apartment buildings. But when interest rates had shot up, the 7% return that he’d been promised had disappeared. Even though the investment syndicate manager had said that all investments carry risk, Yehuda hadn’t really digested that. Nor had he read through the fine print of the agreements he’d scribbled his signature on. What would happen now, when the deal wasn’t providing flowing cash?

Was that 7% still owed to him? And how did this delay of distributions affect future profit sharing?

Ignored Fine Print

It is extremely common for investors to ignore the fine print. Typically, they get pulled into a real estate deal or other investment based on a slick marketing presentation and after hearing nice things about the investment manager’s performance. Often, a pitch includes hints, subtle or not so subtle, that if potential investors don’t get a move on, they will miss out on the opportunity. When the financial sun is shining, some investors jump into even complex deals with simplistic expectations for a smooth, profitable ride despite lackadaisical due diligence.

A World of LPs and GPs

But taking investment shortcuts is usually a mistake. Small differences in operating agreements and prospectuses can translate to huge differences in investment risks and rewards. One example that recently crossed my desk was related to how investment profit splits are structured. In a typical real estate deal, the investors, also known as limited partners (LPs), give money to a managing or general partner (GP), who is responsible for finding and managing the deal. Profits are split, say, 70%/30%, a ratio that is in favor of the LPs, since they are taking virtually all the financial risk.

In further deference to the financial risk the LPs are taking, most GP-led deals are structured so the GP does not earn their share of profits (also known as the promote, performance fee, or carry) before the LPs earn what’s known as a preferred return. Typically, preferred returns are in the vicinity of 7%, meaning that 100% of the first 7% return on investment generated by the asset flows to the LPs. Only when there are profits above the preferred return does the GP get to share in the profits. (Note that we are ignoring compounding in this article and the accompanied table to keep the math simple.)

Favoring LPs

Building in a preferred return favors LPs in two significant ways: First, it allows the LP to get money out of the deal more quickly, improving the LP’s cash flow and lowering their risk exposure. A preferred return also places a hurdle above which the GP must reach in order for them to profit-share. If a deal does not generate profit above the preferred return, the GP’s right to collect promote is worthless, so GPs are incentivized to generate high returns in order to beat the preferred hurdle and earn their promote share of the profits.

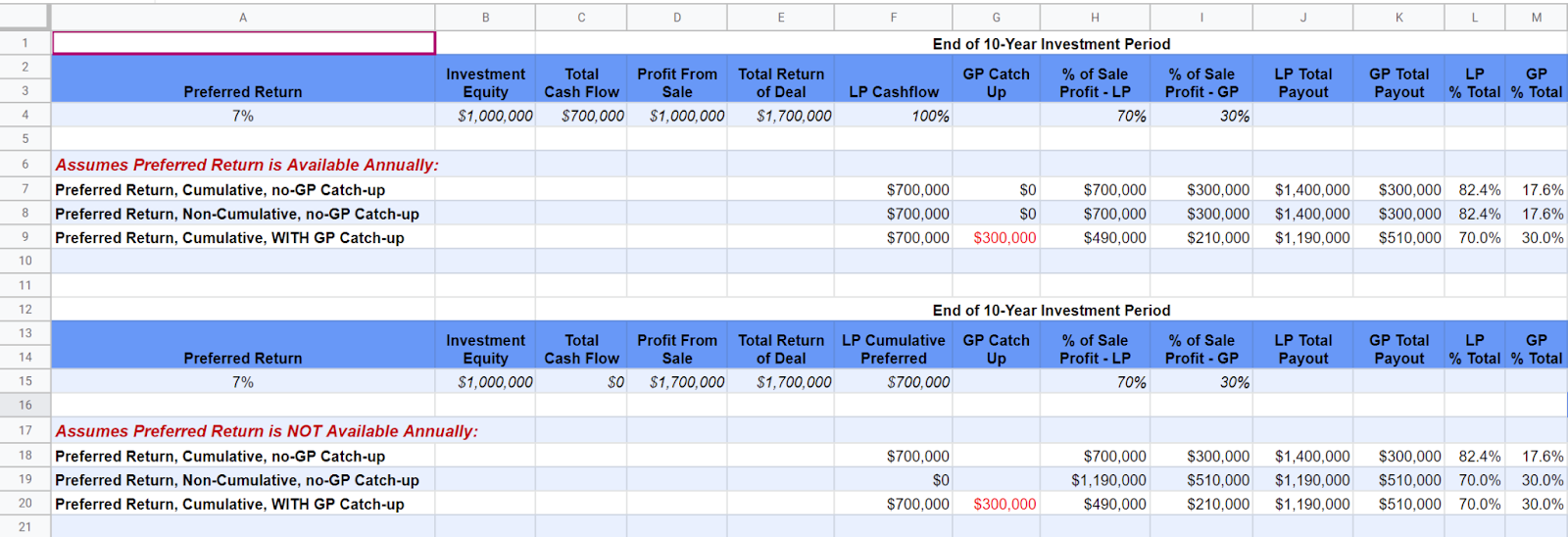

Say a deal with $1 million of equity invested is structured with a 7% preferred return and a 70/30 promote split (see table, row 4). The property ends up generating $70,000 in cash flow annually for 10 years and is then sold with an additional $1 million in profit (after outstanding debt and repaying the original equity). Typically, the LP would collect 100% of the $700,000 in ongoing cash flow as preferred return. Then, with the preferred return out of the way, the additional million in profit is split 70/30 (this is the scenario shown in row 7).

The Catch

Because the LP gets 100% of the preferred return plus 70% of any remaining profits, the actual split between LP and GP of total income earned ends up being 82/18, not 70/30 (cells L7 andM7). Some GPs therefore may add a “GP catch-up” (G9) to tilt cash flow back to their favor once a preferred return has been paid out to LPs. In this catch-up scenario, after the LP takes 100% of the first $700,000 earned as preferred return, the GP gets 100% of the next $300,000 as a catch-up to equalize the payout back from 100/0 to 70/30.

Shift in the Fine Print

This is all a bit “mathy,” but there’s real money involved here. With this catch-up going 100% to the GP, only $700,000 of additional profit remains to be split 70/30. As long as there is money for a catch-up, the LP/GP split is a true 70/30, not the 82/18 of a more traditional structure. And while this is perfectly legitimate when properly disclosed, LPs should at least note, beforehand, that a catch-up spelled out in the fine print can cost them real money (J7 vs. J9).

Cumulative Rights Aren’t a Given…

Getting back to Yehuda’s case, another detail clarified in the fine print of a partnership agreement is what happens if the 7% preferred return does not show up year after year for some reason. Does the preferred return accumulate in arrears, or is it forgone? I think it’s relatively uncommon, but some GPs specify that preferred returns do not accumulate. This structure may increase GP profits at the expense of the LP in some scenarios where performance is worse than expected. Non-cumulation can also create some bizarre incentives for a GP to simply withhold available distributions.

And Make a Real Difference

In the first scenario above, $70,000 is available every year and note how rows 7 and 8 offer identical payouts. But in scenario 2, where the same $1.7 million in total combined deal profit is earned but only all the way at the end, the non-cumulative deal in row 19 earns the GP $210,000 more than the cumulative structure in row 18. The GP gets 30% of the entire $1.7 million instead of just the million earned above the preferred—more money for providing LPs a less advantageous performance!

Different, Not Right or Wrong

Note that the non-cumulation payout is identical to the traditional cumulation structure in scenario one (rows 7 and 8) and identical to a GP catch-up in the second scenario (rows 19 and 20). There are also scenarios in which the catch-up is better for the LP versus the non-cumulation and vice versa, but both are much less advantageous for the LPs versus a more typical structure offerign a prffered with accumulation and no catch up.

The main takeaway is that the fine-print details of investments make a big difference. GPs will typically offer whatever structure they think they can get, and sometimes they hold the upper hand. Either way, it’s on LPs to at least know what they are being offered.