Being responsible for $10 million was something new for Shira Bitton. She’d recently become the controller of a fast-growing company that kept significant amounts of cash on hand for payroll and purchasing materials. Her predecessor had used a tiny local bank for all the company’s needs; this was the convenient choice which also earned the company slightly higher interest than what large national institutions offered. But Shira wondered whether using an insignificant bank was prudent. Because her company was a large customer, the local bankers and tellers were extra friendly and helpful, but the primary purpose of a bank is keeping cash safe and accessible. Is money deposited into a small bank safe? How can you ensure the security of banked cash?

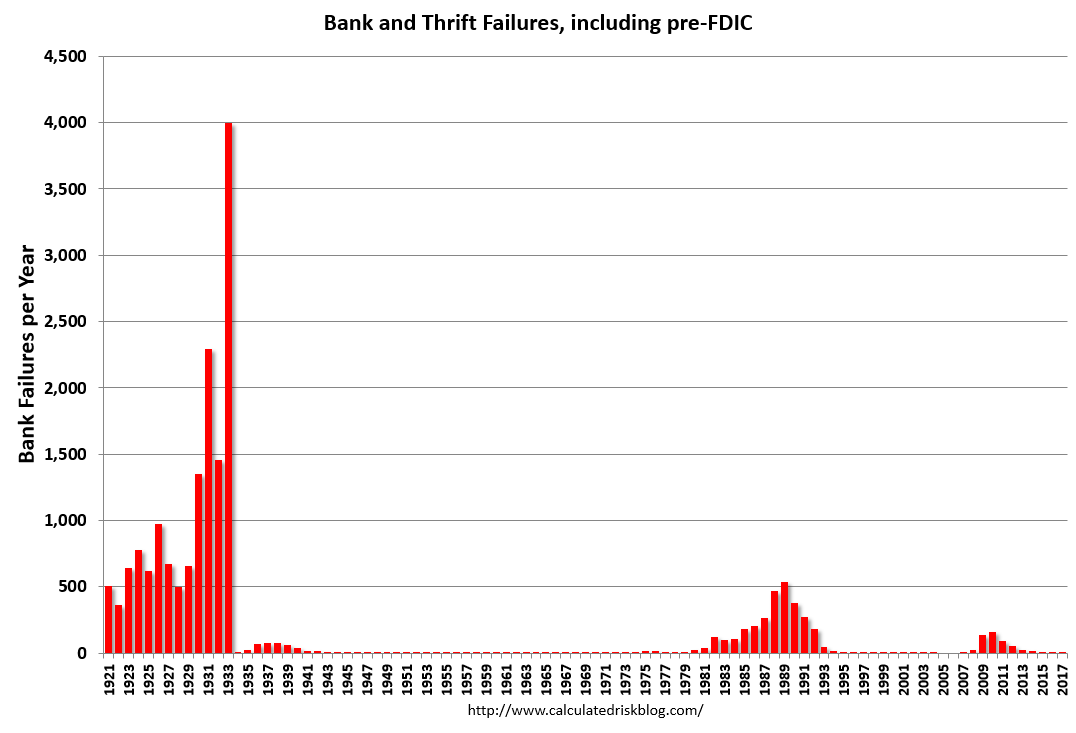

Bank Collapses Used To Be Common

“Money in the bank” is supposed to be a sure thing. This expression is ironic considering how common bank failures have been throughout history. In the United States, hundreds of banks failed every year in the 1920s. At the start of the Great Depression (early 1930s), over 9,000 banks closed their doors, wiping out 5% of all the money deposited into banks across the country! Since then, all banks have been obligated to have government-backed insurance on their deposits (from the Federal Deposit Insurance Corporation, i.e., FDIC). While banks still go bankrupt, they do so much less frequently, and insurance covers virtually all the losses. The catch is that because the coverage is limited (to $250,000 per person, per account), large depositors like Shira’s company are still at risk should their banks fail. But bank failure isn’t related to the size of the institution; in fact, Shira’s tiny bank may be less likely to collapse than a much larger one.

{kind=link}

Bank’s Money Is Mostly Loaned Out

Understanding bank failures and FDIC insurance is easier when you consider how banks earn their profits. Bankers “borrow” money at a low rate from one group—depositors, and lend that same money out to others—the borrowers, at a higher rate, earning a “spread.” Say a group of depositors put $1.1 million into Smiley Savings Bank and receive 2% annual interest, costing the bank $22,000 ($1,100,000 x 2%). Smiley’s bankers than lend $1 million to various borrowers at 5% annually (keeping $100,000 in cash to cover overhead and depositor requests for money back). This process earns Smiley a gross profit of $28,000 ($1,000,000 x 5% = $50,000 less the $22,000 paid to depositors). This arrangement works out well for everyone, assuming Smiley is careful and only approves strong loans backed by sufficient collateral. But, especially during boom times, the bank’s lenders may throw caution to the wind and make some loans that will never be repaid. That’s when things at Smiley Bank start falling apart.

Bank Runs Can Wipe Everyone Out

Say 10% of Smiley loans are such that can’t be collected. As borrowers start defaulting, the bank runs low on cash, and word gets out that Smiley has only 90¢ in assets backing each dollar of deposits. Without FDIC insurance, Smiley Bank may implode entirely even though only 10% of the loans defaulted. Once trust in a bank is shaken, everyone tries to withdraw all their money at once. This situation is known as a bank run, when depositors rush to withdraw their funds from a shaky financial institution. The problem is that, even in good times, Smiley Bank only has about $100,000 of depositors’ cash available on hand; the other $1 million was loaned out and can’t be collected for years. Therefore, if even a tiny percentage of depositors withdraw their savings at the same time, any bank can be crippled. Without cash, the bank will be shuttered, unable to collect and repay even the remaining 90¢ on the dollar that remains in good standing. The risk of a bank run is the same for all banks, regardless of the size of the institution.

FDIC Insures Deposits Up To $250,000

Devastating bank runs often occurred in the olden days, but today, any financial company that accepts deposits—from tiny to gargantuan—is obligated to participate in the FDIC insurance program, run and guaranteed by the Federal Government. Each bank pays a small percentage of its assets into an insurance fund which covers any insured losses that may arise from a bank failure. To keep losses low and trust in the system high, the FDIC monitors banks for risky lending and has the power to shut down imprudent institutions. Should a failure occur, the FDIC handles the dissolution of the bank, guaranteeing any covered losses while protecting those assets that are still collectible. Thanks to FDIC insurance, the average American who deposits well under the $250,000 FDIC limit can bank anywhere without giving thought to the safety of the institution.

Expanding FDIC Coverage

During the financial crisis of 2008, FDIC insurance limits were raised to $250,000, more than enough for the vast majority of people. However, it’s easy for wealthy families to protect millions in cash because FDIC limits are per person, per account category, and per insured institution. Say Mr. Cohen has $2 million sitting in a personal checking account at Santander. Should the bank fail, the FDIC would cover only $250,000 of the $2 million. The Cohens can quickly expand their coverage to the whole amount deposited by adding more people, more account types, and more institutions.

First, $250,000 can be placed into an individual checking account in Mrs. Cohen’s name. An additional $500,000 can be put into a joint account in both of their names, expanding their coverage to $1 million. (Each personal account gets $250,000 coverage, and the joint account, which by FDIC rules is a separate type of account than an individual account, provides coverage of an additional $250,000 per named owner.) They can then open the same three accounts (two individual and one joint) with Harmony Bank (a separately insured institution) to double their coverage to the whole $2 million. And so forth.

While it’s a bit of a pain to maintain multiple accounts, because of electronic linkages, it has become easier to shift funds back and forth even between different banks. Therefore, even those fortunate enough to have millions in cash can keep them all within FDIC protection pretty easily. But companies and organizations, which may need to keep many millions on hand, can’t rely on FDIC insurance. We explore how large depositors, companies, organizations, and the super-wealthy ensure the safety of their cash here Protecting Cash Above FDIC Insurance.