Deena Morgan appreciated the 401(k) match offered by her boss. The question was how to invest the money sitting in her account. At an enrollment meeting, the presenter kept talking about an option called target-date funds (TDF), which he said could be used not only to save for retirement, but even to pay for simchos!

What are TDFs, why are they so popular, and how should investors use them to grow wealth?

Set and Forget

TDFs are fabulous tools. These unique mutual funds have actually been around for decades, but in the last 10 years their usage has exploded. Although most TDF assets are held in retirement accounts, all investors should give them real consideration. TDFs offer regular folks a simplified, affordable, and powerful path to grow wealth over many years. They are actually designed so that investors can “set and forget”—as long as you select the appropriate funds, you can safely ignore them for years or even decades!

Gliding on Predictable Tracks

It may sound wild to abandon your money to the whims of a faceless money manager. But think about getting on a subway. As long as you know where it’s headed, you can snooze until it approaches your station. That predictability is basically what TDFs offer amateur investors. Every mutual fund is a pot of money managed professionally with the aim of reaching a predetermined goal. And the objective of every TDF is to chug along its “track,” shifting over time from a very aggressive to a very conservative portfolio.

We’ve discussed all-in-one funds which combine portfolios of varying risk in a single package. TDFs are also “one and done” options but with a twist: they progressively become less aggressive the closer it gets to the predetermined target date. The premise of all TDFs is that most investors with short-term objectives need to invest very conservatively, while those investing money for decades can afford to invest with more risk potential. The pot of money is placed on a track that begins aggressively and over the decades moves closer and closer to a very conservative retiree’s portfolio.

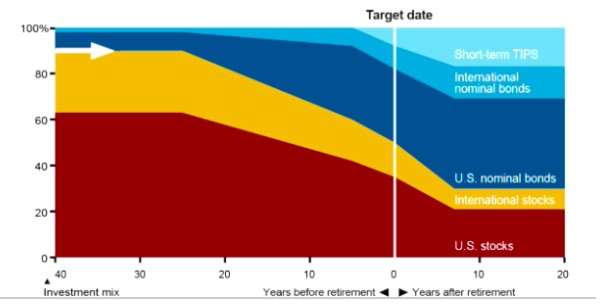

From 2020 to 2040 and Beyond

Consider, for example, Vanguard’s Target Retirement 2040 Fund (ticker VFORX). This fund invests according to an asset-allocation strategy designed for investors planning to retire around the year 2040 (the target year). VFORX’s asset allocation will become more conservative over time, meaning the percentage of assets allocated to stocks will decrease while the percentage of assets allocated to bonds will increase. The “glide path” is the predetermined risk/reward tradeoff track that the manager will follow over long periods of time (see chart).

In 2020, with 20 years remaining to VFORX’s preset 2040 target date, the fund has about 80% of its money in stocks (red and yellow in the chart) and just 20% in much safer bonds (the blue shades in the chart). In 2030, 10 years to the target date, the fund’s managers will invest 65% in stocks and 35% in bonds, while on the target date in 2040, the investments will be evenly divided between stocks and bonds. Over the next few years, the pool of money will be shifted down to a conservative 30-70 breakdown favoring bonds.

In 2020, with 20 years remaining to VFORX’s preset 2040 target date, the fund has about 80% of its money in stocks (red and yellow in the chart) and just 20% in much safer bonds (the blue shades in the chart). In 2030, 10 years to the target date, the fund’s managers will invest 65% in stocks and 35% in bonds, while on the target date in 2040, the investments will be evenly divided between stocks and bonds. Over the next few years, the pool of money will be shifted down to a conservative 30-70 breakdown favoring bonds.

If no change is made by the investor (Deena), the glide path predetermines her portfolio for life. The investment structure at and beyond the target retirement date can confuse investors who didn’t pay attention before they entered the “train.” A 50-50 split upon retirement means that the pot can still fall in value significantly if the stock market goes bonkers. And even a post-retirement exposure of 30% may be more than some retirees want. The assumption built into the glide path is that people will use their accumulated money over many years and not withdraw it all in a lump sum.

Be Prepared for Bumps

And therein lies the primary danger in simply getting on the TDF “train.” The “conductors” of the funds follow the tracks, laid based on what research shows works well for most long-term investors. This systemization enables them to offer solid money management for a very low cost. And indeed, TDFs have been very successful for the most part. But the tracks may follow a journey some are unprepared for. During the great financial crisis of 2008, for example, many elderly TDF investors were shocked to find out how exposed they were to the stock market.

Those who want to lower the risk in their TDF portfolios can simply supplement its bond holdings via another mutual fund or select a fund whose target date is sooner (thereby speeding up the de-risking process). Some savvy 401k companies are beginning to offer customized, lower-risk versions of TDFs for those who want an even more leisurely ride. But adding complexity to the equation negates much of the benefits of TDFs. For the most part, these unique mutual funds work well because people don’t mess around with them.

TDFs for Simcha Savings

Although the target dates for these funds are primarily designed for retirement, they can also be used effectively as simcha funds. Like retirement, simcha saving tends to be a multi-decade affair, as is the subsequent spending period. Parents can begin shoveling money into a fund dated around the time their eldest will be of age. Then they can keep adding and removing funds as the situation demands.

One caveat here, though, is taxes. Unlike retirement, which offers vehicles for dealing with investment taxes, simcha saving doesn’t. There are multiple ways to address this, which I hope to explore at some point down the road.