The blessing of arichus yamim is much degraded if spent in poverty, and financial planning for seniors is vital and challenging. Even if a couple retires with a nice chunk of money, making that pot last till 120+ is hard.

The “Silver Years” Challenge

Say a couple in their mid-60s has $1,000,000 saved up and plans to live modestly on an annual sum of $75,000 (above what they get from Social Security). At that rate, they’ll run out of money in 13 years or so (1,000,000 ÷ 75,000 per year = 13.3 years). While investing all the money in secure government bonds can supply about another 10 years of withdrawals, because of inflation, it’ll likely still not be enough to give them the financial security they seek.

So, while $1,000,000 may sound like a fortune, in the context of replacing a steady salary, it’s not. The challenge is how to maximize a nest egg permanently and securely. In an ideal world, retirees would have 20-30 times their annual income needs saved up. With a pot that size, it’s fairly easy to live off just dividends and interest without touching the principal. But many seniors will have saved far less than that and must seek Plan B alternatives.

Introducing SPIAs: Income for Life

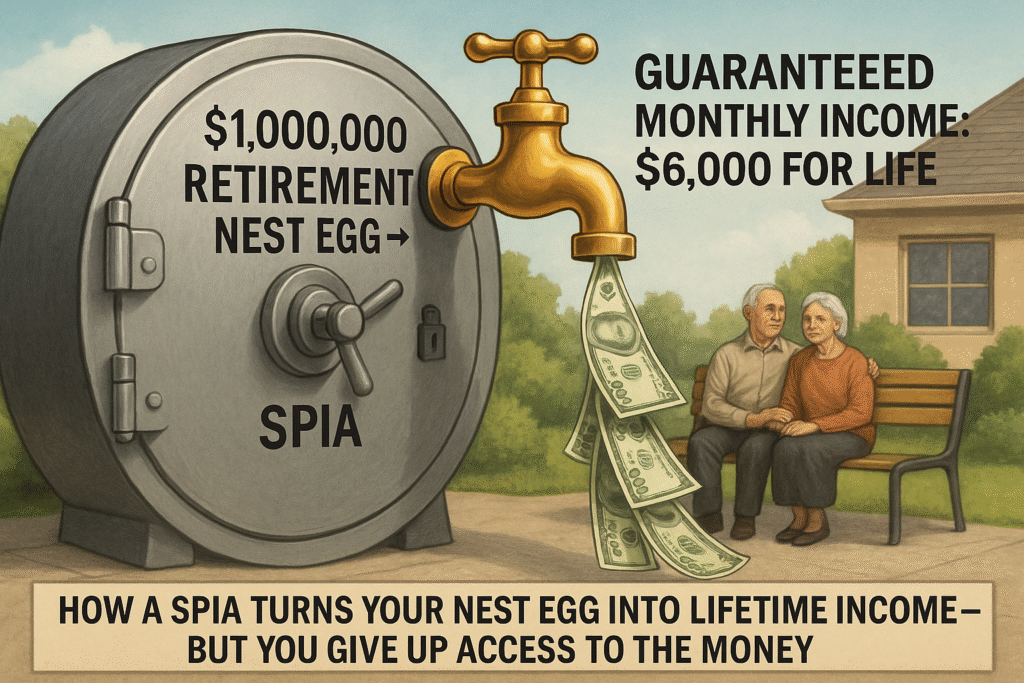

One underutilized tool to avoid running out of money in old age is a fixed-income annuity or a SPIA (single premium income annuity). An SPIA is a type of insurance policy where, in exchange for a one-time payment, a life insurance company guarantees an income for the life of the person or couple protected.

For example, a retiring couple can give their $1,000,000 to an insurance company, which would then be obligated to send them about $6,000 monthly for as long as either one of them lives. (The larger the amount put into the SPIA, the larger the income.)

You can play around with some scenarios here.

So a SPIA converts a $1,000,000 nest-egg into $72,000 of guaranteed annual income (about 7.2% of the $1,000,000). Compare this with the income from a government bond portfolio of just $50,000 annually (about 5% which is what long-term treasury bonds are yielding in mid-2025), i.e. a third less income than what a SPIA provides. As long as they choose a reliable insurance company, a couple can enjoy a more comfortable retirement with a secure SPIA “pension,” guaranteed for life.

But… The Big Catch

But, of course, there’s a catch. The massive difference between a $1,000,000 SPIA policy and a $1,000,000 bond portfolio is that once handed over to an insurance company, the premium of a SPIA is gone! Should the retiree be hit by a truck on the way home from the insurance agent’s office, his descendants would get nothing, whereas had he bought a portfolio of bonds, every penny would be left to his estate.

And, even if a couple enjoys a long life, they may need access to cash for an uncovered medical need or to help a child, and because all their retirement money was placed into an irrevocable insurance policy, they can’t do anything about it.

Most people can’t get past the thought of losing control of all their money and the possibility of the life insurance company making a “killing” should they pass on quickly. Because of this emotional but understandable perspective, SPIAs are unpopular despite their significant capabilities to minimize elder poverty.

Insurance Realities

The life insurance companies aren’t being greedy when taking control of the principal of an SPIA; it’s what they require to provide the valuable security retirees seek. Consider the opposite case, where instead of dying right after buying their $1,000,000 SPIA, the retirees live until 120, collecting a total of $3,960,000 in annual payments from their SPIA policy ($72,000 x 55 years). Generating that much guaranteed money from $1,000,000 isn’t easy for the life insurance company either!

Bonds don’t pay that much, and even if they wanted to, insurance companies aren’t allowed to base their guarantees on higher-potential but risky investments like stocks and real estate. It’s only by taking the excess money earned from people who die sooner than expected that the companies have money to pay those who live longer than expected. That’s the simple financial reality of insurance.

SPIA: Life Insurance in Reverse

This SPIA arrangement sounds like life insurance in reverse because that’s precisely what it is! Annuities are the mirror image of life insurance: one protects from the financial problems of dying early, and the other from dying “late” (i.e., outliving available assets). A SPIA is the annuity equivalent of term-life insurance, transparent and straightforward, leaving little room for errors or hidden commissions.

Although it can be painful, one Plan B approach for a secure retirement income is putting a good chunk of money into a SPIA. Indeed, recognizing that buying an annuity need not be an all-or-nothing proposition, i.e., annuitizing only a part of your nest egg, may be the way to get the best of both worlds: the security of an ongoing income stream and continued access to some still large sum of money that can be invested and used as a yerusha or for some other important goal.

Complicated Annuities Require a Second Opinion

Although SPIAs are pretty straightforward, seniors should shop around and seek second opinions, as they should before committing to any significant financial commitment. Also note that, in addition to SPIAs, insurance companies offer a dizzying array of other annuity types with investment and “rider” options, which sometimes make economic sense but literally require an actuary to comprehend.

As with cash-value insurance, agents make much larger commissions for the bells-and-whistles type of annuities, and there is little transparency as to the fees hidden within them. Due to their complexity and the potential for biased pitches, any potential purchase of these products requires a professional review from an unconflicted insurance expert.